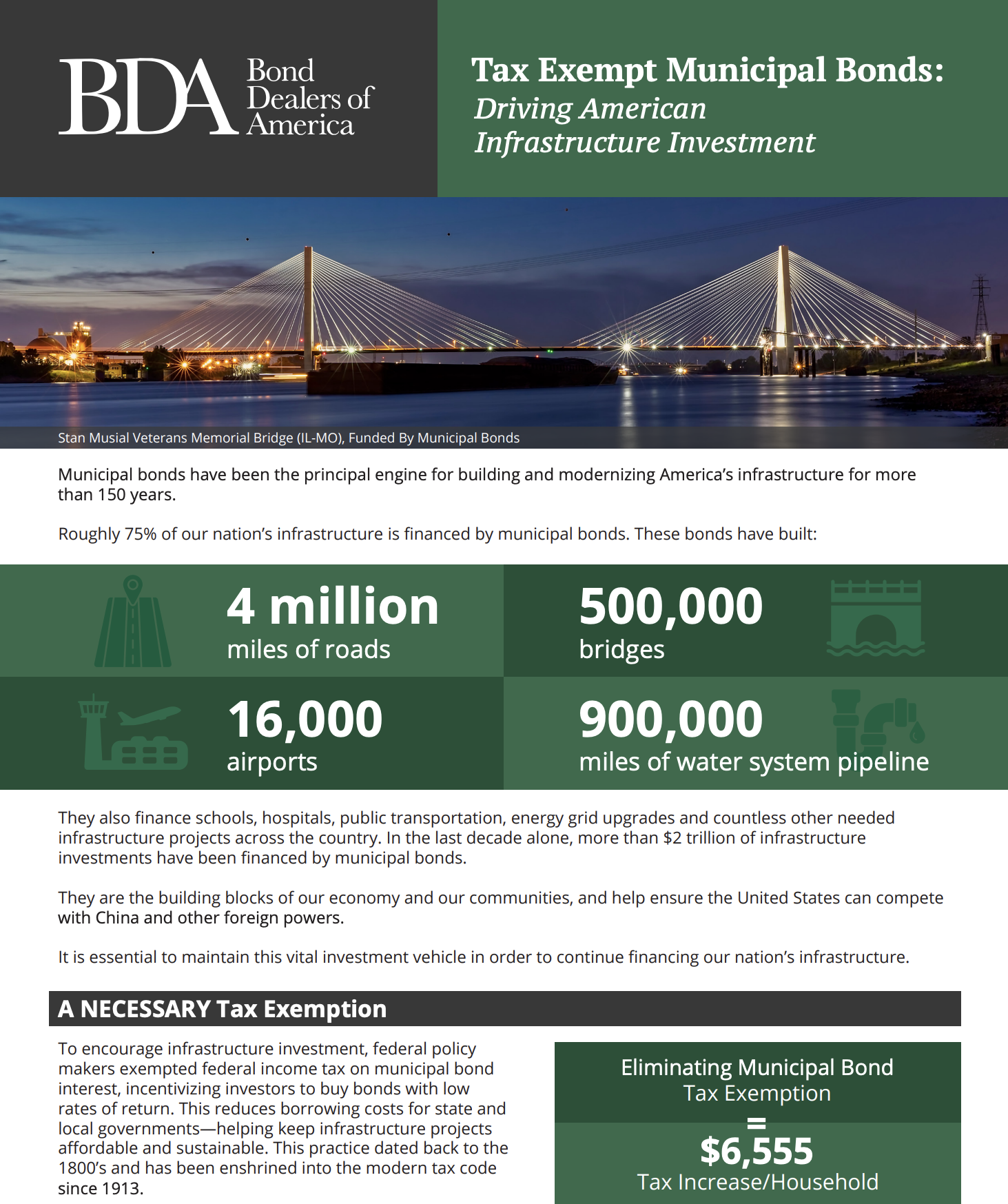

The Bond Dealers of America (BDA) deploys a variety of advocacy and grassroots tools to influence the policy-making process and promote a more efficient fixed-income market. Regulatory authorities in Washington, D.C. recognize the BDA as an authority on technical issues and market trends. Through a variety of events and forums, our members have the opportunity to meet regulators and legislators to discuss market and business challenges. Our federal Political Action Committee (PAC) supports legislators who work to advance policies that improve the fixed income markets.

Federal Legislative and Regulatory Priorities & Accomplishments

Funding Fights Dominate DC

What’s New:

In what could have been a catastrophic and tenure-defining month for Speaker Johnson, last week quickly turned into a success as Congress passed a flurry of key legislation. Under growing pressure from the White House and Senate, the House approved a funding bill for the Department of Homeland Security, sans immigration enforcement, ending a 76-day partial government shutdown.

Background:

Following the vote, the House also passed the Senate budget reconciliation outline that creates a pathway to fund immigration enforcement for the rest of Trump’s term. The budget resolution instructs Congressional Committees to draft legislation authorizing $70 billion to pay for ICE and the Border Patrol for roughly the next three years.

Leadership had to work overtime to keep their caucus in line as the budget outline calls for vast spending with little-to-no offsets. The vote was held open for an extended period, with Johnson and his whip team actively lobbying conservatives on the House floor to switch their vote in support of the measure. In the end, their efforts succeeded with the package passing the House 215-211-1.

It is unknown at this point what the Speaker may have promised the conservative holdouts in return for supporting the measure, but passage of the funding stopgap and the reconciliation outline amidst an aggressive pressure campaign on the floor has made it more likely that Republicans will craft a “reconciliation 3.0” at some point this year to help calm conservative angst.

As noted, Congress is not planning to pay for the next reconciliation package, but the consensus is that a “reconciliation 3.0” would be used as a vehicle for sweeping cuts that were not fully achieved last year. This will likely include social safety net cuts, as well changes to federal tax expenditures.

The BDA, along with our friends in the Public Finance Network have continued to advocate for key tax priorities such as the restoration of tax-exempt advance refundings, and the small issuer exception, while simultaneously building of last years successes in defending the tax-exemption.

We still feel heading into next year, there is a window of opportunity for these bond provisions to advance whether in a post midterm end lame duck tax bill, or potentially in a bipartisan package next year in what will likely be a divided DC.

GSE Reform Stalls

What’s New:

BDA staff met with the U.S. Department of Treasury’s Office of Capital Markets leadership to discuss the status of the Administration’s GSE reform efforts following President Trump’s public statements on the potential for an IPO of Fannie Mae and Freddie Mac.

Background:

The meeting focused on the status of any potential changes to the GSE’s, how the changes could impact the market, and what, if anything, Treasury is doing following the President’s pronouncements.

Key Takeaways Include:

- In May 2025, Trump posted on Truth Social that he was giving “very serious consideration” to bringing them public and would be working with Treasury Secretary Scott Bessent, Commerce Secretary Howard Lutnick, and Federal Housing Finance Agency (FHFA) Director William Pulte on a decision.

- Treasury began work on conceptualizing what this would look like, and noted they worked to “boil the ocean” in an effort to ensure all angles were considered.

- At this point, the Office of Capital Markets is not focused on GSE reform, and noted they are taking a wait-and-see approach to see if the President directs any further action.

Treasury staff remain interested in the MBS market and how any potential changes to the conservatorship status would impact the market.

Their questions focused on:

- The concern about losing the federal backstop, and the need to ensure it remains;

- Preserving the TBA market, and how privatization would impact it; and

- Market reaction to UMBS.

Remote supervision

What’s New:

FINRA last year issued a request for comment around a regulatory review related to the “modern workplace,” including a review of remote supervision rules. BDA’s letter in response focused on outlining the manner in which fixed income traders and others are supervised and made a case for greater flexibility around remote work and supervision.

FINRA’s consideration of these issues is consistent with BDA’s requests to both FINRA and the MSRB to further amend remote supervision regulation. BDA members met with senior FINRA staff on this issue in September, and FINRA indicated that they are drafting amendments to remote supervision rules. We expect to see a proposal soon.

The MSRB recently approved a proposal to amend Rule G-27 related to supervision. Under the proposal, the current 30-day exception from treatment as a branch office or OMSJ for locations other than a primary residence would be extended to 60 days. The proposal would also clarify the definition pf “structuring.” BDA’s letter to the Board was generally supportive. The next step is for the MSRB to send the proposal to the SEC for final consideration.

Background:

FINRA in 2024 finalized changes to FINRA Rule 3110 related to remote supervision. The release announced that FINRA was terminating the temporary, COVID-related remote work relief that had been in place since 2020 and establishing a new, permanent regime for remote work involving the new concept of “Residential Supervisory Location.” It also announced the creation of a new voluntary “Remote Inspections Pilot Program.” On May 10 the MSRB issued their own changes to MSRB Rule G-27 designed to comport the MSRB’s treatment of remote work and supervision with FINRA’s changes.

Unfortunately, the new, more flexible rules do not include traders or employees who “structure” transactions, and a priority for BDA is to incorporate those categories of employees in a more flexible regime. One issue that has arisen with respect to the MSRB rule changes is the divergent treatment of public finance bankers who may also work as Municipal Advisors and the employees of non-dealer MA firms. Another is the need for traders’ homes to be designated as Offices of Supervisory Jurisdiction (OSJs).

FINRA finalizes amendments to gift rule, MSRB following

What’s New:

The SEC recently approved amendments to FINRA Rule 3220 related to gifts and non-cash compensation. FINRA raised the annual limit on gifts subject to the Rule from $100 to $300 and made other changes, including:

- Excluded certain personal, bereavement, and promotional items of de minimis value from the Rule;

- Specified that the Rule does not apply to gifts to retail customers; and

- FINRA can now grant exceptions to the Rule under certain circumstances.

The FINRA changes took effect on Monday, March 30, 2026. Changing the gift rule was a priority raised in our latter to FINRA last year on regulatory modernization. As reported above, the MSRB has informed us that they plan to issue their own proposal to amend their gift rule to bring it into line with FINRA’s changes likely next month.

On May 1 the MSRB filed with the SEC proposed amendments to MSRB Rule G-20, the MSRB’s gift rule.

MSRB Release on SMMP Definition

What’s New:

The MSRB recently issued draft amendments on reforming and updating MSRB Rule D-15, which defines the term Sophisticated Municipal Market Participant (SMMP). The proposal would remove the requirement that dealers obtain an affirmation from Registered Investment Adviser customers before considering them as SMMPs. The proposal would maintain the requirement of a minimum of $50 million of total assets for most SMMPs but would raise the threshold for municipal entities (issuers) to $100 million. BDA filed a letter in support of the proposal but opposing the $100 million threshold for state and local governments.

At its recent meeting, the MSRB Board failed to approve any changes to Rule D-15.

Background:

In 2023 the MSRB issued a concept release which proposed to eliminate the requirement for SMMPs to provide affirmations. In our comment letter in response, BDA supported the elimination of the affirmation requirement.

SEC Rule 15c2-11

What’s New:

The SEC has announced that they will amend SEC Rule 15c2-11 to specify that the Rule applies only to equity securities, not to fixed income. They proposed an effective date 60 days after publication in the Federal Register, or May 18, 2026. BDA is preparing a comment letter in support of the proposal.

Background:

In 2021 the SEC announced for the first time that Rule 15c2-11, a long-established rule in the OTC equity markets, also applies to quotations in fixed income securities. SEC staff then issued a temporary staff-no-action letter effectively exempting many bonds from the Rule if they meet certain criteria. The Rule requires traders, before publishing a quotation to a quotation medium, to review certain issuer financial information and ensure that information is available publicly.

In 2024 the SEC issued a new staff no-action letter with respect to the application of SEC Rule 15c2-11 to quotations for fixed income securities excluding municipals. The no-action letter effectively exempts many fixed income quotations from the Rule as long as the securities being quoted meet certain criteria. The newly issued letter does not have an expiration date.

BDA wrote to SEC Chairman Atkins last year asking the Commission to reverse their 2021 decision to apply SEC Rule 15c2-11 to quotations in fixed income securities. (Municipals and governments are explicitly exempt from the Rule.) A group of BDA members met with SEC Commissioner Mark Uyeda in the fall on the issue, and Uyeda signaled informally that rather than simply reversing the Gensler decision, the Commission is planning to formally amend Rule 15c2-11 to explicitly exclude fixed income products from the Rule. BDA staff have also talked informally with Chairman Atkins about the issue, and he indicated a willingness to meet with BDA members on the issue. In December the House Financial Services Committee approved H.R. 3959, the Protecting Private Job Creators Act, legislation which would block the application of Rule 15c2-11 to fixed income products.

Principal trading prohibition

BDA is preparing a request to the SEC to provide interpretive relief related to the principal trading prohibition of the Investment Advisors Act (IAA). The IAA generally prohibits registered Investment Advisors (IAs) from engaging in principal transactions with their customers without first obtaining authorization. For decades, the SEC has interpreted that provision as requiring customer authorization for each principal transaction. BDA intends to ask the Commission to revise their interpretation so that one-time or annual authorizations that apply to all principal trades would satisfy the requirements of the statute.

Financial Data Transparency Act

What’s New:

A joint agency rulemaking, the first formal regulatory action in implementing the Financial Data Transparency Act (FDTA), was released in 2024 by the OCC, Fed, FDIC, NCUA, CFPB, FHFA, CFTC, SEC, and Treasury. The agencies have proposed to require securities issuers to use both Legal Entity Identifiers (LEIs), a system of entity identification, as well as Financial Instrument Global Identifiers (FIGIs). FIGI is an ostensibly less proprietary system of securities identifiers which was developed as an alternative to CUSIPs. BDA raised several concerns in our response to the proposal. The agencies were supposed to have completed their joint rulemaking by the end of 2024. That did not happen. However, there are indications that a final joint agency rule is imminent. After that happens, the SEC will begin drafting rules to implement reporting requirements related to their areas of jurisdiction. One question that has arisen recently is whether language-based artificial intelligence makes structured data disclosure obsolete.

Background:

In 2022 Congress enacted the FDTA as part of the National Defense Authorization Act. The Act is designed to promote the interoperability of data provided to financial regulators. The regulatory proposal would establish certain cross-agency data standards. One element, a standard for financial instrument identification, would use the Financial Instrument Global Identifier scheme instead of CUSIP.

The FDTA will, among other provisions, require municipal issuers to publish financial disclosure statements in a machine-readable format which will allow software to identify common data elements within the statements. There is a four-year implementation period from the date of enactment. The statute requires the SEC to develop a “taxonomy,” a collection of data items associated with tags that will make the documents

machine-readable. Issuers generally remain opposed to the FDTA.

One concern about the proposal is that at some point in the future the SEC may expect dealers to police municipal issuer compliance with the FDTA standard as current regulations do with respect to issuer continuing disclosure. Second is that the FDTA initiative could impose costs on the MSRB as the market’s disclosure repository which would be borne predominantly by dealers.

FINRA amendments related to reporting principal transactions

FINRA has amended Rule 6730 related to transaction reporting to provide additional flexibility around allocations by dually registered BD/IAs. When FINRA withdrew its one- minute trade reporting initiative last year, they announced that they would continue to pursue one element of the initiative related to streamlining the way dually registered BDs/IAs report block trades made by the BD and allocated to IA accounts. Currently, each allocation must be reported to TRACE individually. Under the change FINRA has announced, BDs would have the choice to continue reporting allocations as under current rules or to report the number of allocations but not each one individually. The change takes effect on June 8, 2026.

MSRB proposes amendments to rule governing interdealer trade comparisons

The MSRB has filed with the SEC proposed changes to MSRB Rule G-12 related to comparing interdealer trades in securities which are not eligible for automated comparison at DTCC, typically because they do not qualify for a CUSIP. The MSRB has proposed to retire outdated guidance related to the Rule and incorporate certain existing guidance into rule text. BDA will respond by the comment deadline.

Advocacy Feature